There are many reasons why you may want to know whether you can take your pension early in Ireland. The answer depends on a number of factors, including when you took out the policy and how much money was put into it by your employer. If it has been more than 10 years since you started working for Goldman Sachs or if the value of your pension is less than 80% of its original value, then yes – it is possible to cash in your pension early without suffering any penalties from the Irish government. However, it’s always best to consult an advisor before making any decisions about taking out any policies with an insurer or financial institution as there could be legal implications too (i.e. if they’re caught doing something illegal).

Can I take my pension early ireland

Can I take my pension early ireland?

Absolutely. If you are over 55, and have been drawing a social security pension for at least 10 years, then it is possible to take your pension early. The rules are slightly different though depending on whether or not you are living in Ireland:

- If you live in an EEA country (EU member states), then there is no restriction on taking home more than one year’s worth of your state pension at once; however, if this money is withdrawn from elsewhere (ie outside of Ireland), then it will be subject to any applicable withholding tax or equivalent levy by HMRC

- If you live in another jurisdiction outside Europe (including Australia), then withdrawing any amount from your state pension before reaching age 60 will result in a 10% penalty being applied

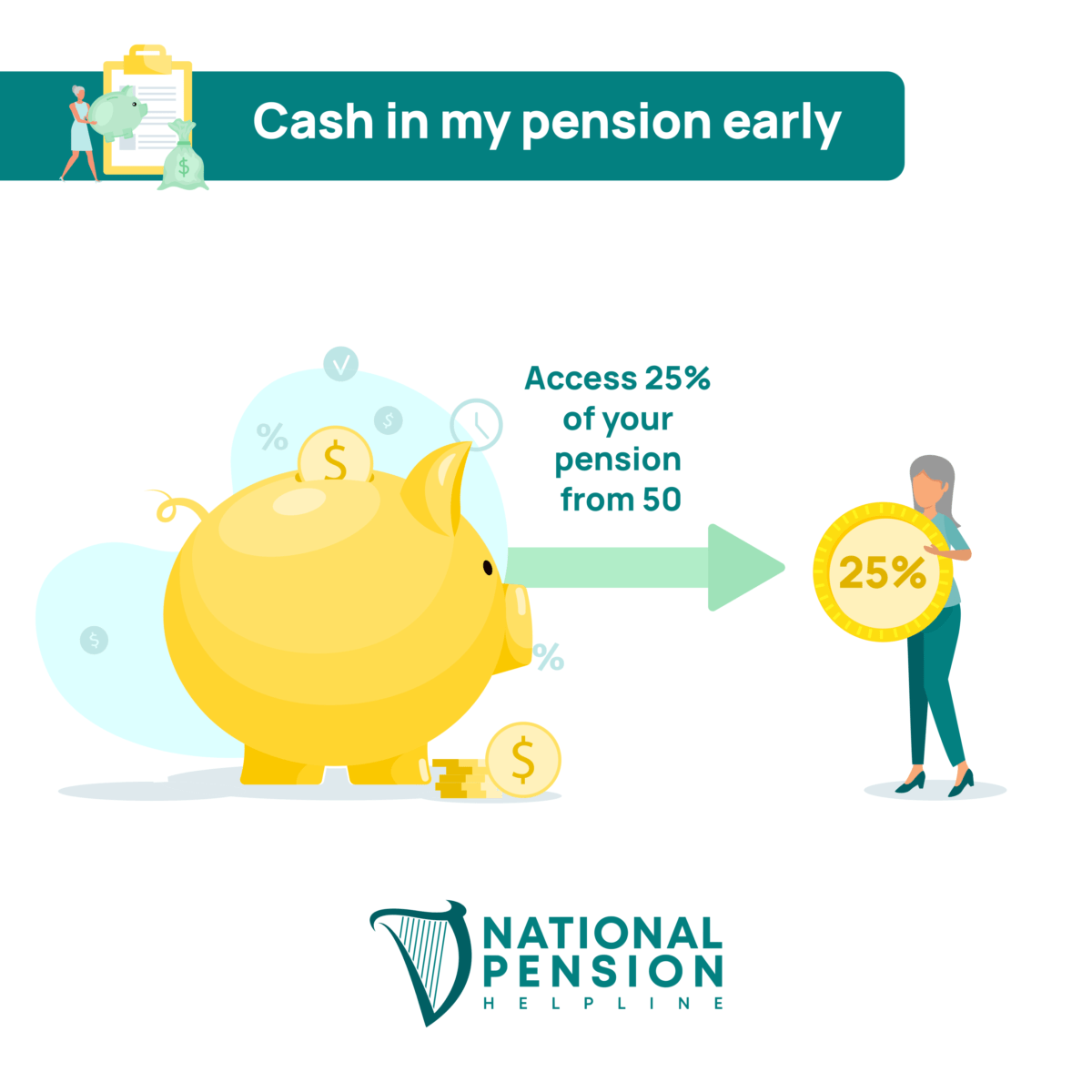

Can I cash in my pension in ireland

If you are over the age of 50 and have been a member of Irish Friendly Society for at least five years, you can cash your pension early. The amount that you can cash varies depending on when you start Cash in my pension and where in Ireland it was purchased. You will also need to pay an early withdrawal penalty fee if this is the first time that you have ever withdrawn funds from an Irish Friendly Society pension plan (this fee is €250).

If people move from one country to another within Europe, there may be restrictions on how much money they can take out of their pensions while working abroad – so make sure to check with them first!

What is the best age to take your pension

The best age to take your pension is the age at which you can afford to do so. You can take your pension at any time, but there are certain guidelines that apply:

- If you have worked less than 10 years, then it will be subject to tax on withdrawal. This means that if you take out more than £3,500 per year (or £250 per month), then HMRC will charge interest and penalties on top of this amount until they receive payment from yourself or another source of income.

- If you have worked between 10-15 years, then withdrawals are not taxed as long as they are paid directly into an approved scheme provider (e.g., TPD Ltd).

Take a 15-year term policy for 100,000 and save 15,000 per year. You will have money to help pay for college or any other expenses.

If you have a 15-year term policy for 100,000 and save 15,000 per year, you will have money to help pay for college or any other expenses.

The amount that can be withdrawn from your pension is based on how much you earn and how long you have been in the scheme. The maximum amount that can be withdrawn is 85% of your final salary (i.e., 20% if 55 years old).

Allow yourself to begin planning for your retirement at any age.

It’s never too early to start planning for your retirement. You may have been working since you were 18, but it doesn’t mean that you should stop saving and investing now—you can still start planning for the future when you’re older.

The first thing that I recommend is opening up a Roth IRA account in which to fund your savings. This way, every year when taxes are due (or even just once per month), some money will automatically be deposited into this account without any additional paperwork or hassle involved. The other option would be putting aside regular monthly deposits into an old-fashioned 401(k) plan or traditional IRA; both of these options give access to tax-deferred growth until retirement age (65 years old), so there’s no need for panic if something goes wrong on your end during this time period!

Conclusion

If you’re thinking about taking your pension early, you should think hard. You might be able to use it to fund a college education or pay off debt. But remember: life events like getting married, having children and buying a house can affect when you’ll start withdrawing funds from your retirement account. If those changes cause you to want more money sooner than later—or if something unexpected happens—your options may change.